NZ Insurance Market Update

Jess Hunt Executive General Manager Broking Branches

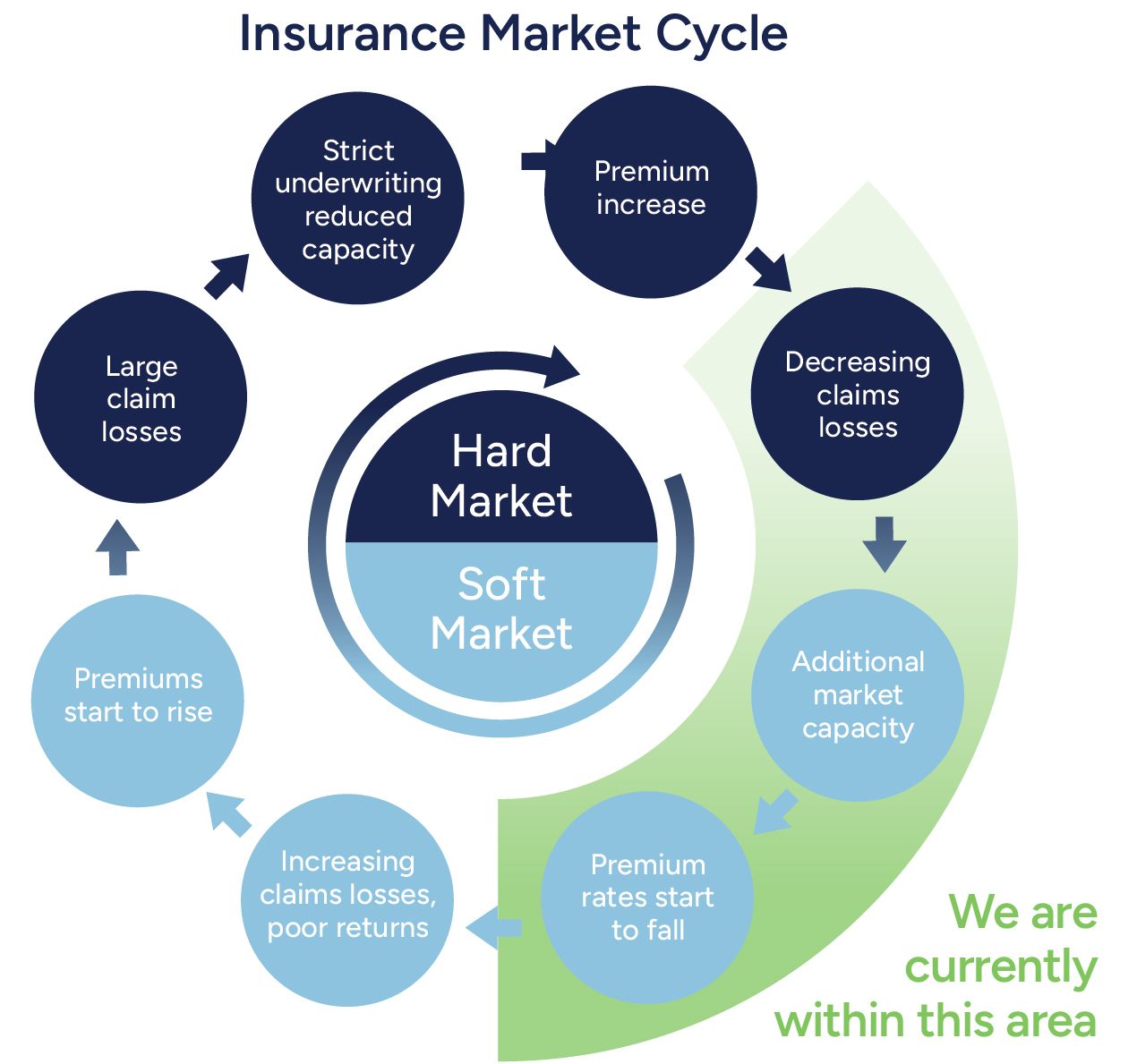

Market overview: A soft insurance market driven by unique dynamics

Since our last update in November, the New Zealand Insurance market has shifted considerably and is now experiencing a prolonged soft cycle. This trend, in line with global trends, is marked by falling premiums, increased competition and a greater appetite for growth amongst insurers.

While this market creates a landscape that strongly favours buyers and presents opportunities for businesses to review their cover, negotiate better terms, and potentially reduce costs, it’s important to recognise that this isn’t a typical soft market; unique and complex factors are at play.

- A prolonged period of low claims activity, improving insurer profitability.

- Greater capacity and appetite among existing insurers, to write more risk

- New insurers entering the market, increasing competition

- Economic pressure on businesses, promoting changes in insurance strategies

While the environment is favourable, certain sectors still face challenges. Clients with poor risk management practices, high claims frequency, or those operating cool stores with EPS or in earthquake-prone buildings are unlikely to attract widespread interest from insurers or see any relief in premiums. For these businesses, strategic engagement with their Rothbury broker is essential.

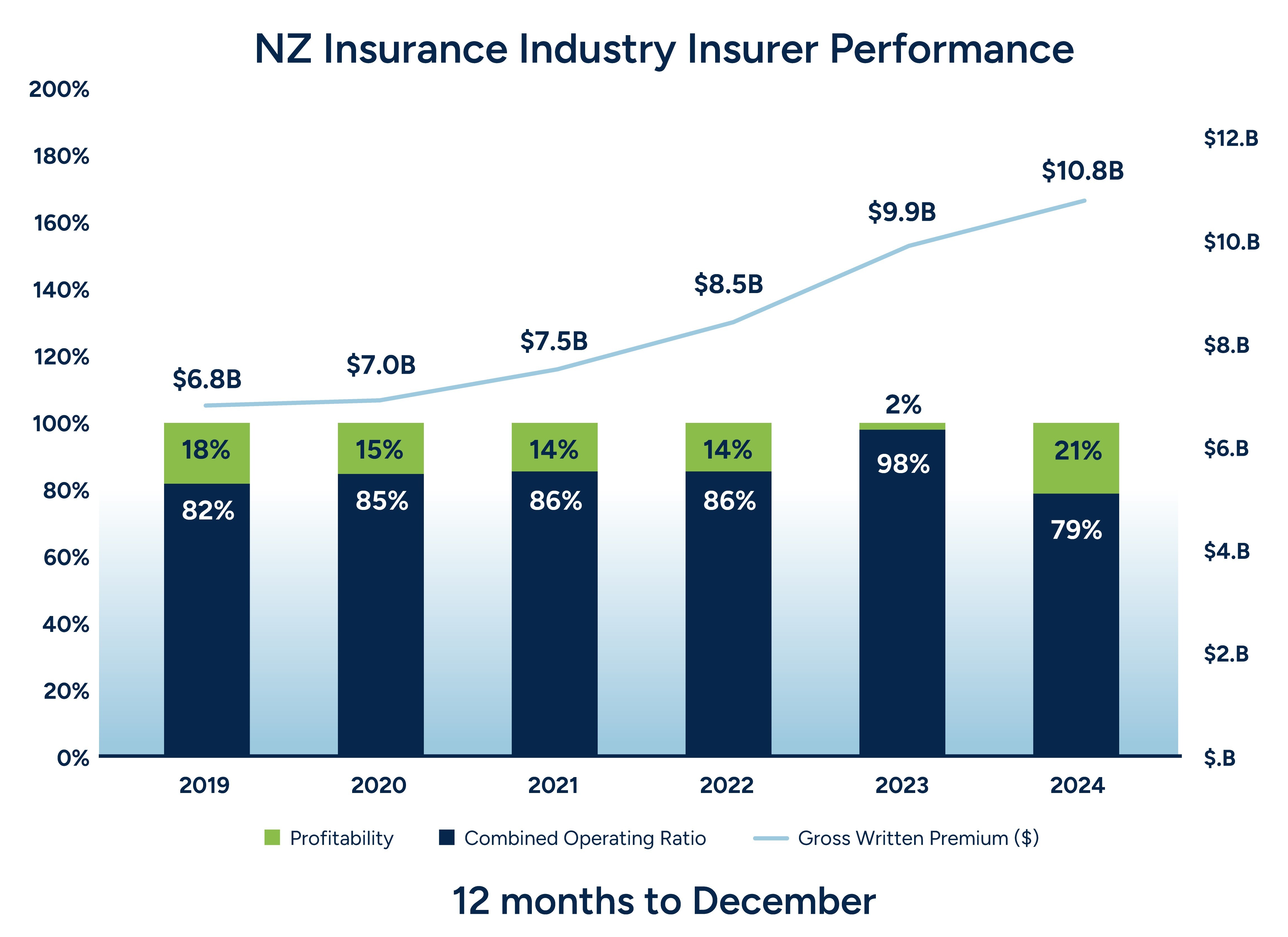

Market recovery and insurer appetite

Following the significant weather events of 2023, insurers have rebuilt capital reserves and restored market confidence, driven by premium increases in 2023 and early 2024, an unusually benign claims environment, and stabilising reinsurance costs.

As a result, insurers are actively seeking growth, with new entrants, including those backed by Lloyds of London, heightening competition. Some existing insurers are broadening their appetite, expanding into new industry sectors and offering sharper pricing, broader coverage, and more flexible terms – particularly for clients with strong risk profiles.

Rate movement and coverage trends*

As insurers compete more aggressively, we’re seeing

notable shifts in pricing and coverage across key

product lines:

- Property insurance rates have dropped by up to 13%, marking five consecutive quarters of reductions.

- Casualty (liability) rates are down 5%, with competitive pricing across both primary

and excess layers.

- Financial & Professional lines (including D&O) have fallen 10%, with flexible retentions and long-term agreements in some cases available.

- Cyber premiums are down 10%, with more innovative coverage options.

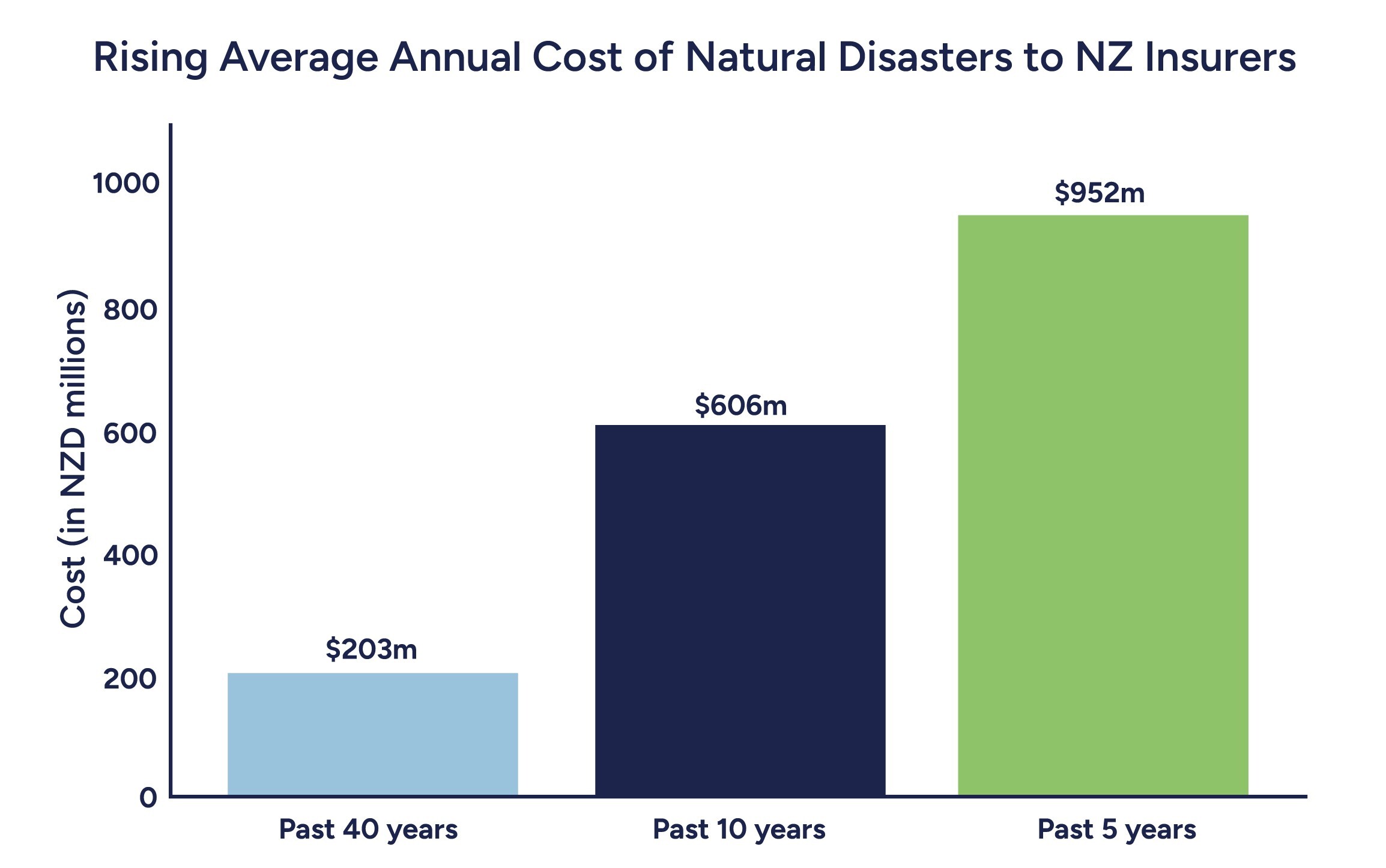

At the same time, upcoming changes to the Fire and Emergency New Zealand (FENZ) levy in 2026 are

expected to place upward pressure on total insurance spend for commercial property, rural infrastructure, and other high-value assets like boats and aircraft. Although the FENZ levy is applied separately from the premium, it still contributes to the total cost of placing insurance and should be factored into budgeting decisions.

This is more than just a rate story – it reflects a shift in mindset. As the market evolves, it’s important to consider not just price, but also how you can strengthen your risk position and coverage quality.

*These pricing trends are based on general market observations for medium to large businesses. Actual rates may vary by sector, region,

or individual risk profile.