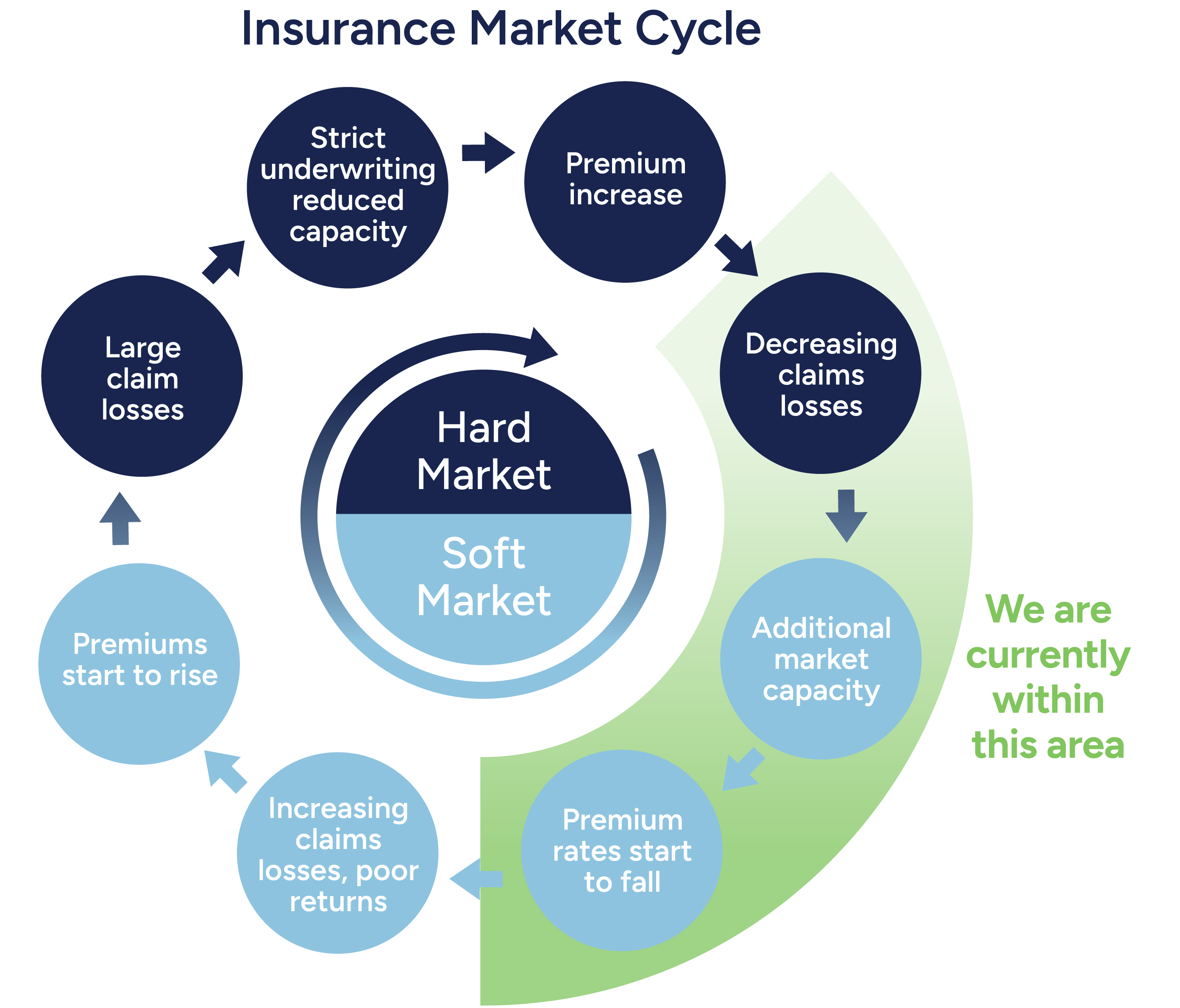

Market recovery and insurer appetite

There is now more capacity to offer home insurance across the country, as insurers recover from the financial impact of Cyclone Gabrielle and the North Island floods in 2023.

One key reason is the stabilisation of reinsurance pricing. After those major events, global reinsurers raised their rates sharply, which drove up premiums for homeowners. But the market has since adjusted. Insurers such as IAG and Suncorp have reported strong profits and improved performance, attracting more investment and increasing competition.

That said, in some high-risk areas - such as parts of Wellington exposed to earthquake and coastal risks, or low-lying regions like South Dunedin prone to flooding - insurers are taking a more cautious approach. Policies in these regions may exclude specific risks or come with higher excesses. This approach helps insurers keep cover available while managing their exposure to severe natural events and reflects a broader shift toward pricing based on individual property risk.

Premium rises begin to settle

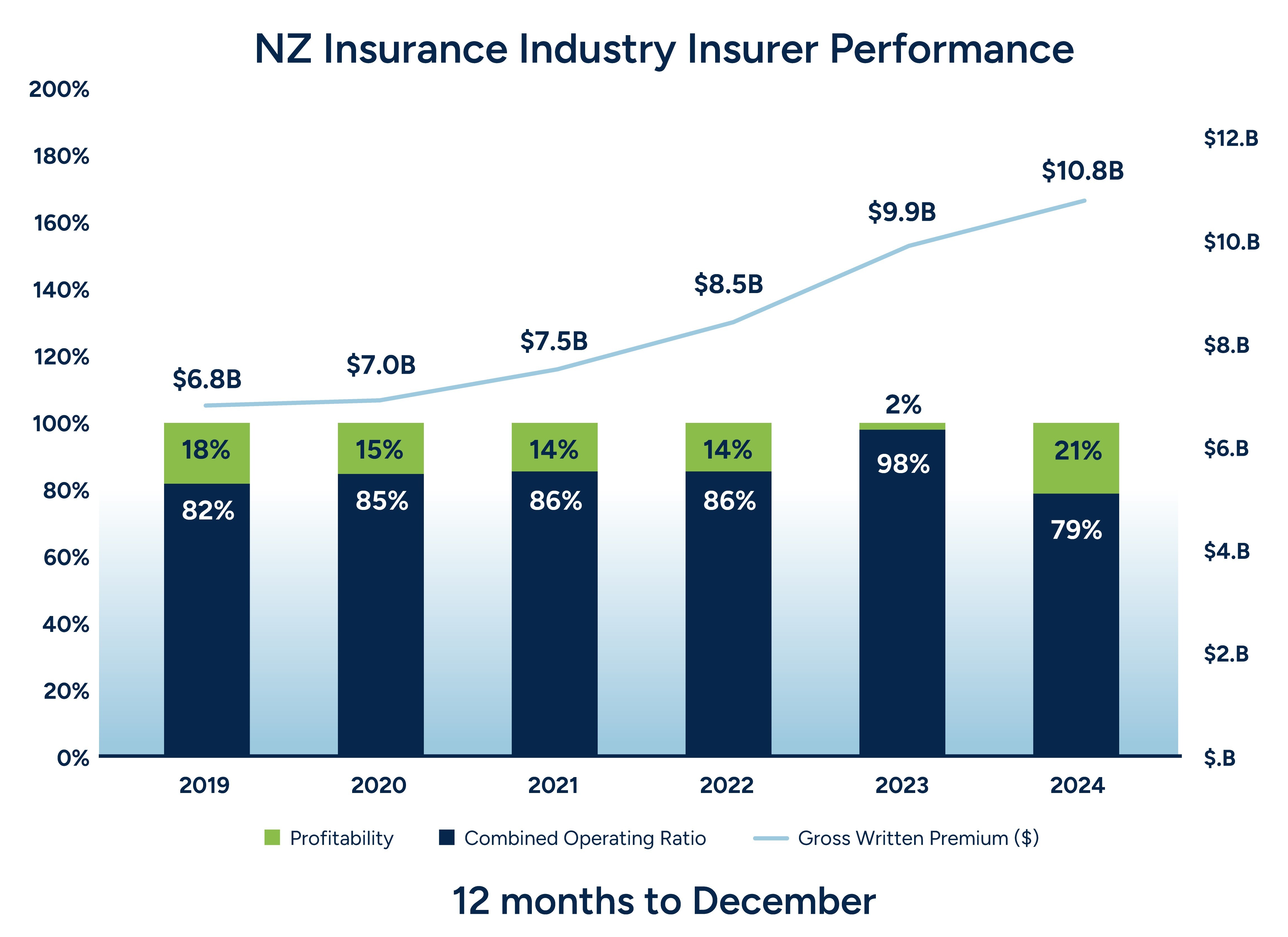

According to Suncorp New Zealand chief executive Jimmy

Higgins, the sharp increases in home insurance premiums are

expected to ease over the next year. He noted that “the market

has stabilised, and future premium rises are likely to track more

closely with general inflation, rather than the steep surges seen

in recent years”. *

Still, pricing varies. Homeowners in higher-risk areas or those

with recent claims may still face elevated premiums and

increased excesses, as insurers continue to manage exposure

carefully.

Meanwhile, motor insurance is showing signs of softening. Many

drivers are seeing better pricing, thanks to fewer claims. Insurers

are increasingly tailoring premiums to individual driver profiles

– like driving history, vehicle type, and location – rather than

applying blanket increases. This means safer drivers may benefit

from lower premiums.

It’s also worth noting that government levies still affect

overall insurance costs. An expected increase to the Fire and

Emergency New Zealand (FENZ) levy in 2026 may offset some

of the benefits of market softening, as taxes and statutory

charges make up a significant portion of your premium.*Source: New Zealand Herald, 15 August 2025

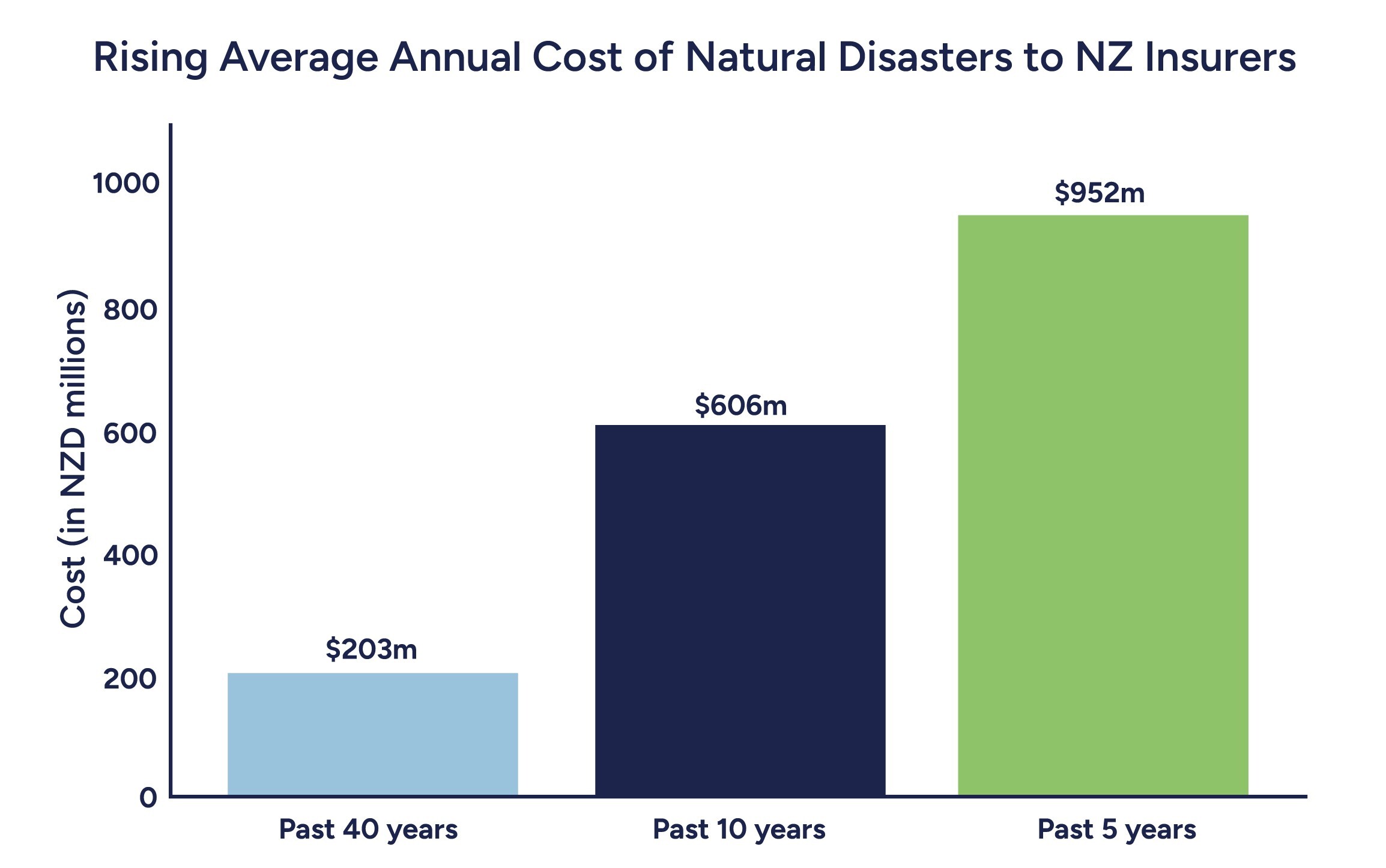

The risks reshaping your insurance

Even in a stabilising market, evolving risks continue to influence how insurers assess and price personal insurance policies. These factors may not drive across-the board increases, but they can affect individual premiums and policy terms:

- Extreme weather: More frequent floods, storms,

and even tornados are now a regular feature of

New Zealand’s climate landscape. These events

reshaping how insurers view risk, especially in

vulnerable areas. As a result, some homeowners

may face higher premiums or find that certain

events – like flooding – are no longer covered in

their policies.

- Vehicle technology: Modern cars are packed

with increasingly complex features such as

sensors, cameras, and advanced driver-assistance

systems – embedded in areas like bumpers and

windscreens. While these features enhance safety,

they also make repairs more expensive and time consuming, even for minor damage.

- Repair cost pressures: While supply chain pressures have eased, elevated costs for building materials, advanced vehicle technology, and skilled labour shortages still continue to influence premium pricing and excess levels.

Together, these pressures highlight why regular policy reviews are essential. Stability in the market doesn’t eliminate the need to check what’s covered and ensure your insurance reflects today’s risks

Getting the best value from your

insurance in the current market

With the insurance market beginning to stabilise, now is a great time for homeowners to review their cover and ensure it reflects today’s risks, costs, and property conditions.

To truly capitalise on current market conditions, your Rothbury broker plays a critical role in this - not just as a placement partner, but as your strategic adviser.

- Check your sum insured: Make sure it reflects

current rebuild costs. Rising construction prices

mean outdated valuations could leave you

underinsured.

- Understand your cover: Review your policy

exclusions – especially for natural disasters –

so you know what’s covered and what’s not.

- Know your property’s risk: Councils are updating zoning and flood maps, and some properties are being reclassified. New home buyers should check council zoning maps and LIM reports for section notices and flood zone status.

- Improve your home’s resilience: Simple upgrades

like flood barriers or roof maintenance can reduce

risk and may help with premiums.

Working with your Rothbury broker can help you assess whether your current insurer and policy continue to be the right fit - and help guide you through any changes in the market.

This report is intended for informational purposes only and does not constitute legal, financial, or insurance advice.

Download the full PDF reportEnquire Now